We accelerate digital business

From Payments Orchestration to Banking Services — all in one unified platform. Infinite possibilities.

ISO 27001 certified — your data security is our top priority.

ISO 27001 certified — your data security is our top priority.

Companies, corporations and financial institutions that already trust us

Trusted by global brands to orchestrate payments and financial services worldwide.

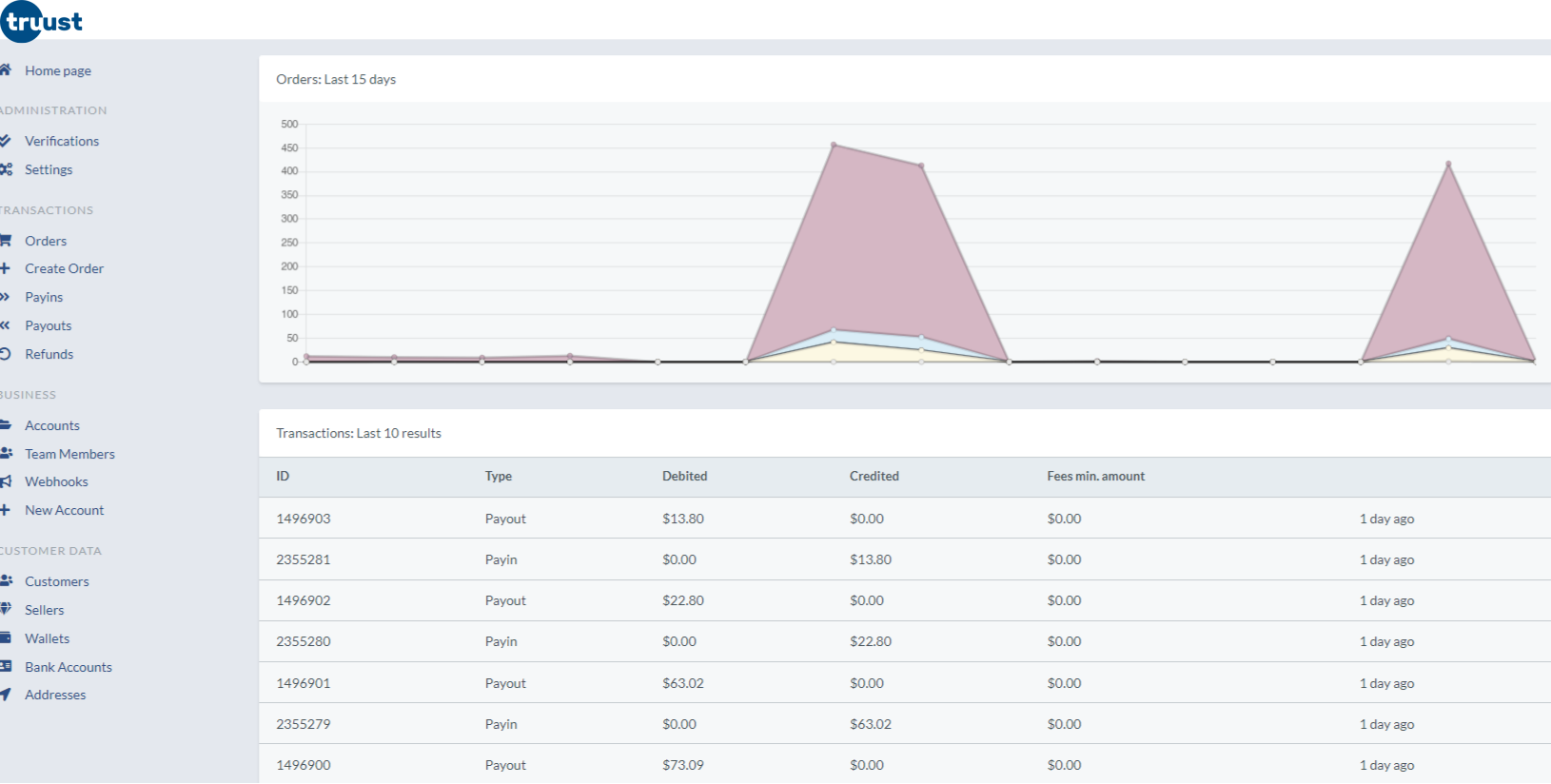

Payment Orchestration

Connect, unify, and control all your payment providers through a single API.

Key benefits:

-

Unified Control: Integrate and manage all payment flows from one place — online, in-app, or in-store.

-

Flexible Journeys: Customize checkout experiences and payment logic across markets and brands.

-

Reliability: Truust API ensures operational resilience and business continuity.

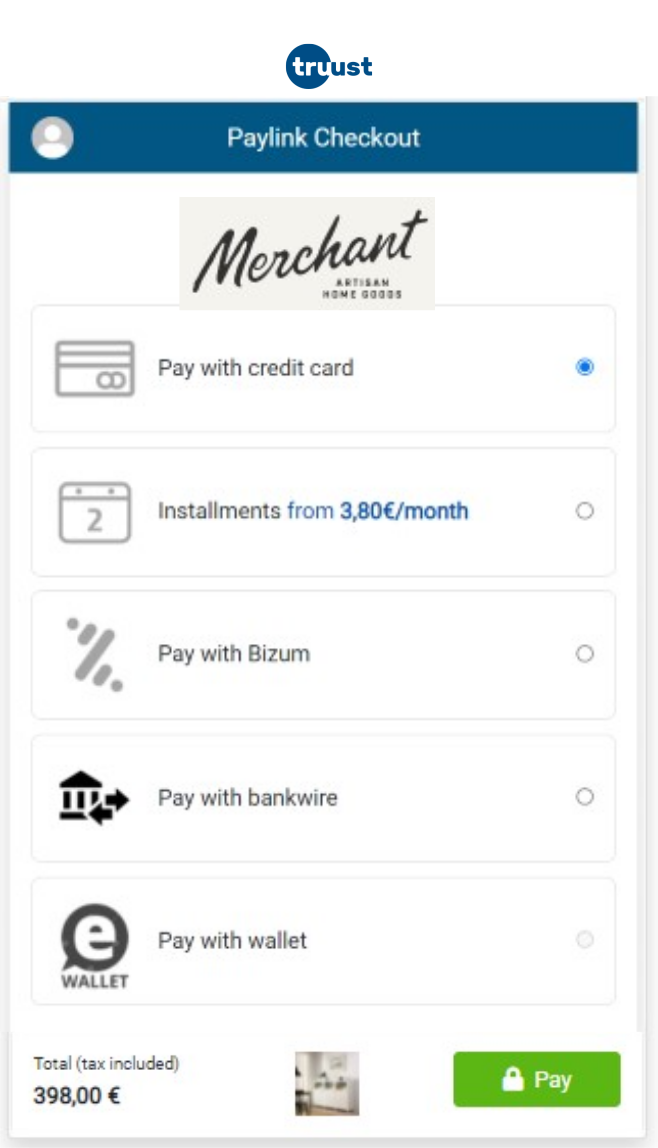

Banking-as-a-Service

Embed regulated financial services directly into your product — without becoming a bank.

Key benefits:

-

Comprehensive Banking Tools: Offer wallets, IBANs, fund transfers, FX, and safeguarded accounts.

-

Trusted Partnerships: We collaborate with licensed banks and fintech providers.

-

Truust Ledger: Real-time reconciliation and tracking of all cash movements.

Innovate your business

Save time and money with Truust. Automate reconciliation, enhance customer journeys with smooth, conversion-optimized checkouts, and unlock actionable insights across all channels.

Get in touch